Raymond Lifestyle announced that Gautam Hari Singhania has been appointed as the executive chairman of the company. Per a regulatory filing, out of the 100 per cent of 4,17,57,480 votes, 86.85 per cent were cast in favour of the resolution while the remaining 13.15 per cent were against the resolution of the appointment. The special resolution proposed in a Postal Ballot Notice dated November 04, 2024, Raymond Lifestyle said, have been passed with the requisite majority.

The remote e-voting commenced on November 05, 2024, at 9.00 am and ended on December 4, 2024, at 5.00 pm. Shareholders were asked to approve Gautam Singhania’s tenure, which is set to span from September 1, 2024, to August 31, 2029. However, concerns were raised by proxy advisory firms, Empowerment Services (SES) and Institutional Investor Advisory Services India (IiAS). According to media reports, they had asked the shareholders to reject the move, citing concerns over governance, transparency, and reputational risks. Per reports, SES also expressed reservations about his simultaneous full-time roles in Raymond and Raymond Lifestyle, the lack of an absolute cap on his variable pay and commission, and unclear restructuring plans.

Meanwhile, IiAS criticised the lack of detail in the proposed remuneration structure, noting the absence of a maximum cap and performance-linked metrics for commission payouts. It also underscored the reputational challenges linked to Gautam Singhania and said that he is undergoing divorce proceedings, during which his wife, Nawaz Modi, has accused him of domestic violence and misuse of company funds for personal gains.

Vikrant Massey’s lavish lifestyle: A sea-facing luxurious house in Mumbai, Rs 1.16 crore Mercedes-Benz GLS, and more

Manika Election Results 2024: Winner, Runner-up, Past Polls Decision, Candidates List & More

Chandankiyari Election Results 2024: Winner, Runner-up, Past Polls Decision, Candidates List & More

Jamua Election Results 2024: Winner, Runner-up, Past Polls Decision, Candidates List & More

Earlier this year, Raymond Group had announced the demerger of the company. It had said that post completion of all formalities for both the Scheme of Arrangement, there will be three listed entities in the Raymond Group i.e. Raymond Limited, Raymond Lifestyle Limited and Raymond Realty Limited.

Mumbai: Two corporate governance advisory firms – Stakeholders Empowerment Services (SES) and Institutional Investor Advisory Services India (IiAS) – have recommended shareholders of Raymond Lifestyle to vote against Gautam Singhania’s appointment as executive chairperson. The proxy advisors cited Singhania’s appointment ahead of the board approval, concerns over remuneration policies and potential “reputational risks” as among the key reasons for the recommendation.

The company is seeking shareholders’ approval for the appointment of Gautam Singhania as the executive chairman for five years from September 1, 2024, to August 31, 2029. The e-voting, which started on November 5, will conclude on December 4.

Raymond did not respond to ET’s queries.

SES said the company went ahead and appointed Singhania as the executive chairman before getting the board’s approval. According to the proxy advisor, “excessive time commitments” due to holding two full-time positions, the absence of an absolute cap on the variable pay and commission, and a lack of clarity on business restructuring are among the reasons for its recommendation.

The lifestyle business of Raymond was demerged into Raymond Lifestyle which was listed separately on September 5. Singhania holds executive positions on the boards of both Raymond and Raymond Lifestyle.

SES said an individual should not hold more than one full-time position unless the directorships are held in companies engaged in similar lines of business.The stock, which listed at ₹2,850 on September 5, has declined 28.5% since then to close at ₹2,026 on the BSE on Monday.IiAS said that Raymond has not provided any details regarding the commission payable to him.

“The proposed remuneration structure is open-ended with limited contours, which limits our ability to estimate aggregate remuneration,” said IiAS in a note to shareholders. “There is no maximum cap on the remuneration, no disclosures on the performance targets required to be achieved for the commission to be paid, nor any clarity on whether malus or clawback clauses have been built into the remuneration structure.”

Promoters held 54.67% stake in the company as of September 30, 2024, while foreign portfolio investors held a 12.63% stake and domestic institutional investors 7.89%.

According to the firm, Singhania is currently undergoing divorce proceedings and his wife, Nawaz Modi, has accused him of domestic violence and alleged that he has used company funds for personal benefits.

“The board has not issued an update since their last statement in December 2023, and it is unclear if it has sought an independent investigation into these accusations,” IiAS said.

Raymond Lifestyle has reported a 69.72 per cent decline in consolidated net profit to Rs 42.18 crore for the second quarter ended September 2024, on account of subdued demand and higher inflationary pressures. It had reported a net profit of Rs 139.33 crore for the July-September quarter a year ago, according to a late night regulatory filing from Raymond Lifestyle, a Raymond Group firm on Tuesday.

Its revenue from operations was down 5.27 per cent to Rs 1,708.26 crore in the September quarter. It was at Rs 1,803.38 crore in the year-ago period.

Total expenses of the Singhania family-promoted firm were down 1.38 per cent to Rs 1,622.95 crore in Q2 FY’25.

Raymond Lifestyle’s total income, which includes other income, was at Rs 1,735.21 crore, down 6.16 per cent.

“Raymond Lifestyle Ltd had a stable quarterly performance amidst subdued demand, weaker consumer sentiment and higher inflationary pressures,” Managing Director Sunil Kataria said.

During the quarter, Raymond Lifestyle’s revenue from the Textile segment, which consists of the branded fabric business of the company, was down 8.48 per cent to Rs 853.52 crore. The decline was “predominantly on account of muted customer demand and ‘Shraadh’ in the month of September. the company said in its earning statement. However, its revenue from ‘Shirting’ fabric, a B2B segment, was up 8.31 per cent to Rs 228.35 crore.

The apparel segment was marginally up around 1 per cent to Rs 441.02 crore in the September quarter. This segment, which has a branded readymade garments business, was driven by new store additions despite subdued consumer demand and challenging market conditions, it added.

Its revenue from ‘Garmenting’ was down 9.28 per cent to Rs 259.60 crore in the September quarter.

The performance of the garment manufacturing business in Q2 FY25 was “impacted by certain delays in shipment dispatches due to logistic challenges,” it said.

During the quarter, Raymond Lifestyle continued its focus on retail expansion and operated 1,592 stores including 129 in Ethnix by Raymond.

“Recent buoyancy has been witnessed at the start of a festive & wedding season. Going forward, we are strategically positioned to capture demand through our retail expansion plans, new product launches and marketing campaigns,” said Kataria.

This is the first quarter result of Raymond Lifestyle, which demerged from the parent company Raymond Ltd and listed on the stock exchanges on September 5 this year.

It has a portfolio of brands such as Park Avenue, ColorPlus, Parx, Raymond Made to Measure, Raymond Ready to Wear, Sleepz by Raymond and Ethnix by Raymond amongst others.

Shares of Raymond Lifestyle Ltd on Wednesday morning were trading at Rs 2,030 per scrip on BSE, down 7.67 per cent from the previous close.

Raymond Lifestyle has reported a 69.72 per cent decline in consolidated net profit to Rs 42.18 crore for the second quarter ended September 2024, on account of subdued demand and higher inflationary pressures. It had reported a net profit of Rs 139.33 crore for the July-September quarter a year ago, according to a late night regulatory filing from Raymond Lifestyle, a Raymond Group firm on Tuesday.

Its revenue from operations was down 5.27 per cent to Rs 1,708.26 crore in the September quarter. It was at Rs 1,803.38 crore in the year-ago period.

Total expenses of the Singhania family-promoted firm were down 1.38 per cent to Rs 1,622.95 crore in Q2 FY’25.

Raymond Lifestyle’s total income, which includes other income, was at Rs 1,735.21 crore, down 6.16 per cent.

“Raymond Lifestyle Ltd had a stable quarterly performance amidst subdued demand, weaker consumer sentiment and higher inflationary pressures,” Managing Director Sunil Kataria said.

During the quarter, Raymond Lifestyle’s revenue from the Textile segment, which consists of the branded fabric business of the company, was down 8.48 per cent to Rs 853.52 crore. The decline was “predominantly on account of muted customer demand and ‘Shraadh’ in the month of September. the company said in its earning statement. However, its revenue from ‘Shirting’ fabric, a B2B segment, was up 8.31 per cent to Rs 228.35 crore.

The apparel segment was marginally up around 1 per cent to Rs 441.02 crore in the September quarter. This segment, which has a branded readymade garments business, was driven by new store additions despite subdued consumer demand and challenging market conditions, it added.

Its revenue from ‘Garmenting’ was down 9.28 per cent to Rs 259.60 crore in the September quarter.

The performance of the garment manufacturing business in Q2 FY25 was “impacted by certain delays in shipment dispatches due to logistic challenges,” it said.

During the quarter, Raymond Lifestyle continued its focus on retail expansion and operated 1,592 stores including 129 in Ethnix by Raymond.

“Recent buoyancy has been witnessed at the start of a festive & wedding season. Going forward, we are strategically positioned to capture demand through our retail expansion plans, new product launches and marketing campaigns,” said Kataria.

This is the first quarter result of Raymond Lifestyle, which demerged from the parent company Raymond Ltd and listed on the stock exchanges on September 5 this year.

It has a portfolio of brands such as Park Avenue, ColorPlus, Parx, Raymond Made to Measure, Raymond Ready to Wear, Sleepz by Raymond and Ethnix by Raymond amongst others.

Shares of Raymond Lifestyle Ltd on Wednesday morning were trading at Rs 2,030 per scrip on BSE, down 7.67 per cent from the previous close.

Raymond Lifestyle has reported a 69.72 per cent decline in consolidated net profit to Rs 42.18 crore for the second quarter ended September 2024, on account of subdued demand and higher inflationary pressures. It had reported a net profit of Rs 139.33 crore for the July-September quarter a year ago, according to a late night regulatory filing from Raymond Lifestyle, a Raymond Group firm on Tuesday.

Its revenue from operations was down 5.27 per cent to Rs 1,708.26 crore in the September quarter. It was at Rs 1,803.38 crore in the year-ago period.

Total expenses of the Singhania family-promoted firm were down 1.38 per cent to Rs 1,622.95 crore in Q2 FY’25.

Raymond Lifestyle’s total income, which includes other income, was at Rs 1,735.21 crore, down 6.16 per cent.

“Raymond Lifestyle Ltd had a stable quarterly performance amidst subdued demand, weaker consumer sentiment and higher inflationary pressures,” Managing Director Sunil Kataria said.

During the quarter, Raymond Lifestyle’s revenue from the Textile segment, which consists of the branded fabric business of the company, was down 8.48 per cent to Rs 853.52 crore. The decline was “predominantly on account of muted customer demand and ‘Shraadh’ in the month of September. the company said in its earning statement. However, its revenue from ‘Shirting’ fabric, a B2B segment, was up 8.31 per cent to Rs 228.35 crore.

The apparel segment was marginally up around 1 per cent to Rs 441.02 crore in the September quarter. This segment, which has a branded readymade garments business, was driven by new store additions despite subdued consumer demand and challenging market conditions, it added.

Its revenue from ‘Garmenting’ was down 9.28 per cent to Rs 259.60 crore in the September quarter.

The performance of the garment manufacturing business in Q2 FY25 was “impacted by certain delays in shipment dispatches due to logistic challenges,” it said.

During the quarter, Raymond Lifestyle continued its focus on retail expansion and operated 1,592 stores including 129 in Ethnix by Raymond.

“Recent buoyancy has been witnessed at the start of a festive & wedding season. Going forward, we are strategically positioned to capture demand through our retail expansion plans, new product launches and marketing campaigns,” said Kataria.

This is the first quarter result of Raymond Lifestyle, which demerged from the parent company Raymond Ltd and listed on the stock exchanges on September 5 this year.

It has a portfolio of brands such as Park Avenue, ColorPlus, Parx, Raymond Made to Measure, Raymond Ready to Wear, Sleepz by Raymond and Ethnix by Raymond amongst others.

Shares of Raymond Lifestyle Ltd on Wednesday morning were trading at Rs 2,030 per scrip on BSE, down 7.67 per cent from the previous close.

But let’s begin by understanding Raymond Lifestyle’s various business segments and its competitors in each of those.

Branded textiles

Raymond is well-known for its worsted suiting fabrics, including poly-wool, all-wool, silk, and other blended fabrics used in making garments such as suits and its shirting fabrics, such as cotton and linen. The company has about a 65% market share in the worsted suiting segment. Competitors in this consumer-facing space include Arvind Ltd and Vardhman Ltd.

Branded textiles are Raymond’s highest revenue contributor, accounting for about 50% of its topline in 2023-24. The company’s branded textile unit reported revenue of ₹3,449 crore for FY24, with an Ebitda margin of 20.5%. The segment is clearly a cash cow for the company.

Branded apparel

Raymond sells apparel under four brands to consumers. Its Raymond Ready to Wear and Park Avenue brands offer formal apparel. ColorPlus offers trendy casual and formal apparel, and Parx sells casual clothing for young people.

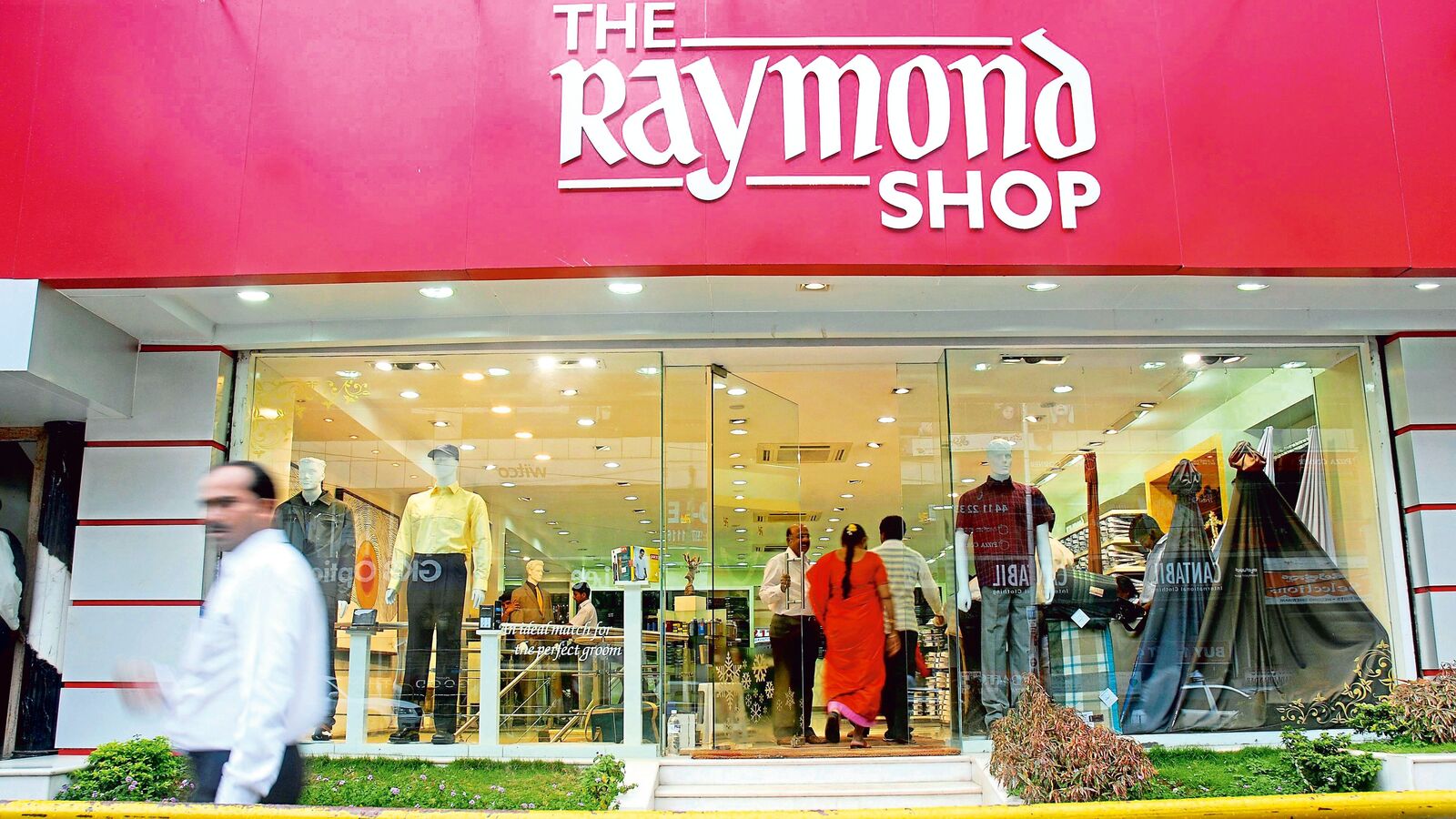

The Raymond Shop, which was started in 1958, has more than 1,100 stores across 380 towns and cities in India, selling these four brands.

The company’s Ethnix by Raymond brand includes ethnic wear such as sherwanis, kurtas, and jackets, which are sold in 114 stores. According to chairman Gautam Singhania, Raymond plans to add at least 100 Ethnix by Raymond stores in FY25.

The company also sells customized suits, jackets, and shirts to customers through its Raymond Made-to-Measure business.

Raymond’s branded apparel business is its second-largest segment. In FY24, it contributed about 23% of the company’s total revenue, with an Ebitda margin of about 11.5%.

Its main competitors in this segment are Arvind, Aditya Birla Fashions and Retail Ltd, Tata Group’s Trent Ltd, and Shoppers Stop Ltd for ready-made apparel; and Vedant Fashions for ethnic wear. However, these competitors also offer women’s wear.

Garmenting

Raymond’s garmenting business supplies ready-made clothes to multinational brands through its subsidiaries—Silver Spark Apparel Ltd for suits, EverBlue Apparel Ltd for jeanswear, and Celebrations Apparel Ltd for shirts. Competitors in this segment include Arvind Ltd, Gokaldas Exports Ltd, and KPR Mill Ltd.

The garmenting business contributed nearly 15% of Raymond’s total revenue in FY24, with an Ebitda margin of 10.3%.

High-value cotton shirting

Raymond Group sells high-quality cotton and linen fabrics to both domestic and international brands. This segment contributed about 12% of its total revenue in FY24, at an Ebitda margin of 11.4%.

Raymond Home

The group launched Raymond Home in 2013 to sell home textile products such as aprons, bedsheets, blankets, bathrobes, comforters, and table linen. Competitors in this space include Welspun Living Ltd and Trident Ltd.

Projections

Raymond Group’s decision to demerge into three listed entities—Raymond Ltd, Raymond Lifestyle Ltd, and Raymond Realty Ltd—and its growth projections reflect its desire to increase market share.

From about a 65% share in worsted suiting fabrics and a 5% share in ethnic men’s wear, the company is committed to increasing its reach by adding more than 650 retail stores over the next 3 years, with over 100 stores specifically for Ethnix by Raymond in FY25. The expansion will be mainly in Tier 1 and 2 cities and selectively in Tier 3 and 4 markets.

The company expects steady revenue growth of 12-15% over the next few years. This, in turn, is expected to double its Ebitda by 2028, per its growth guidance provided at its investor conference on 17 September. The company expects to lower its net working capital days to 60 from the current 76 and generate annual free cash of ₹600-700 crore.

Key financials

Raymond Lifestyle reported net revenue of ₹6,691 crore for the year ended March, adjusted for intersegment elimination and other income of ₹210 crore. With a gross margin of 46%, an Ebitda margin of 16.3%, and a profit-after-tax margin of 7.0%, it reported 97 inventory days and a net cash surplus of ₹227 crore as of 31 March.

The company’s operational return on capital employed was 31.7%, and operational return on equity was 10.4%.

As of September, promoters held about 54.7% of the company’s shares. Foreign institutional investors held about 12.6% of the shares, domestic institutional investors about 7.9%, and the public about 24.8%.

Comparison with peers

Multiple business segments, specifically those focused on men’s wear, make Raymond Lifestyle a unique company. Let’s now consider its key competitors across segments.

View Full Image

.

Raymond Lifestyle has the lowest price-to-earnings (P/E) ratio among its peers, and a better return on capital employed ratio, which shows the company’s profitability and capital efficiency.

Now getting to the question of whether Raymond Lifestyle can trigger a 37% rally. For this, the company is expanding its network of stores and counters as well as its product range, and expects to double its Ebitda by 2028. This is a positive sign for the company at large.

Also, adding ethnic wear, sleepwear and innerwear to its portfolio will increase its revenue and margin in the coming years.

In October, Motilal Oswal Financial Services Ltd, in its initiating coverage report on Raymond Lifestyle, recommended a “buy” on the company’s shares, stating that it expected the company to deliver an 11% compound annual growth rate in revenue and 15% CAGR in profit after tax over FY24-27. It set a target share price of ₹3,200 based on 30x the company’s September 2026 P/E ratio. This implies a return of 37% from current levels.

Note: We have relied on data from www.Screener.in as well as company’s presentation throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Mohit Bhambhani is a seasoned financial professional with over 13 years of experience in the field of financial research and corporate advisory. He also has substantial experience in Indian stock markets. With an analytical approach, he studies the performance of companies deeply, bringing value to the readers.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

But let’s begin by understanding Raymond Lifestyle’s various business segments and its competitors in each of those.

Branded textiles

Raymond is well-known for its worsted suiting fabrics, including poly-wool, all-wool, silk, and other blended fabrics used in making garments such as suits and its shirting fabrics, such as cotton and linen. The company has about a 65% market share in the worsted suiting segment. Competitors in this consumer-facing space include Arvind Ltd and Vardhman Ltd.

Branded textiles are Raymond’s highest revenue contributor, accounting for about 50% of its topline in 2023-24. The company’s branded textile unit reported revenue of ₹3,449 crore for FY24, with an Ebitda margin of 20.5%. The segment is clearly a cash cow for the company.

Branded apparel

Raymond sells apparel under four brands to consumers. Its Raymond Ready to Wear and Park Avenue brands offer formal apparel. ColorPlus offers trendy casual and formal apparel, and Parx sells casual clothing for young people.

The Raymond Shop, which was started in 1958, has more than 1,100 stores across 380 towns and cities in India, selling these four brands.

The company’s Ethnix by Raymond brand includes ethnic wear such as sherwanis, kurtas, and jackets, which are sold in 114 stores. According to chairman Gautam Singhania, Raymond plans to add at least 100 Ethnix by Raymond stores in FY25.

The company also sells customized suits, jackets, and shirts to customers through its Raymond Made-to-Measure business.

Raymond’s branded apparel business is its second-largest segment. In FY24, it contributed about 23% of the company’s total revenue, with an Ebitda margin of about 11.5%.

Its main competitors in this segment are Arvind, Aditya Birla Fashions and Retail Ltd, Tata Group’s Trent Ltd, and Shoppers Stop Ltd for ready-made apparel; and Vedant Fashions for ethnic wear. However, these competitors also offer women’s wear.

Garmenting

Raymond’s garmenting business supplies ready-made clothes to multinational brands through its subsidiaries—Silver Spark Apparel Ltd for suits, EverBlue Apparel Ltd for jeanswear, and Celebrations Apparel Ltd for shirts. Competitors in this segment include Arvind Ltd, Gokaldas Exports Ltd, and KPR Mill Ltd.

The garmenting business contributed nearly 15% of Raymond’s total revenue in FY24, with an Ebitda margin of 10.3%.

High-value cotton shirting

Raymond Group sells high-quality cotton and linen fabrics to both domestic and international brands. This segment contributed about 12% of its total revenue in FY24, at an Ebitda margin of 11.4%.

Raymond Home

The group launched Raymond Home in 2013 to sell home textile products such as aprons, bedsheets, blankets, bathrobes, comforters, and table linen. Competitors in this space include Welspun Living Ltd and Trident Ltd.

Projections

Raymond Group’s decision to demerge into three listed entities—Raymond Ltd, Raymond Lifestyle Ltd, and Raymond Realty Ltd—and its growth projections reflect its desire to increase market share.

From about a 65% share in worsted suiting fabrics and a 5% share in ethnic men’s wear, the company is committed to increasing its reach by adding more than 650 retail stores over the next 3 years, with over 100 stores specifically for Ethnix by Raymond in FY25. The expansion will be mainly in Tier 1 and 2 cities and selectively in Tier 3 and 4 markets.

The company expects steady revenue growth of 12-15% over the next few years. This, in turn, is expected to double its Ebitda by 2028, per its growth guidance provided at its investor conference on 17 September. The company expects to lower its net working capital days to 60 from the current 76 and generate annual free cash of ₹600-700 crore.

Key financials

Raymond Lifestyle reported net revenue of ₹6,691 crore for the year ended March, adjusted for intersegment elimination and other income of ₹210 crore. With a gross margin of 46%, an Ebitda margin of 16.3%, and a profit-after-tax margin of 7.0%, it reported 97 inventory days and a net cash surplus of ₹227 crore as of 31 March.

The company’s operational return on capital employed was 31.7%, and operational return on equity was 10.4%.

As of September, promoters held about 54.7% of the company’s shares. Foreign institutional investors held about 12.6% of the shares, domestic institutional investors about 7.9%, and the public about 24.8%.

Comparison with peers

Multiple business segments, specifically those focused on men’s wear, make Raymond Lifestyle a unique company. Let’s now consider its key competitors across segments.

View Full Image

.

Raymond Lifestyle has the lowest price-to-earnings (P/E) ratio among its peers, and a better return on capital employed ratio, which shows the company’s profitability and capital efficiency.

Now getting to the question of whether Raymond Lifestyle can trigger a 37% rally. For this, the company is expanding its network of stores and counters as well as its product range, and expects to double its Ebitda by 2028. This is a positive sign for the company at large.

Also, adding ethnic wear, sleepwear and innerwear to its portfolio will increase its revenue and margin in the coming years.

In October, Motilal Oswal Financial Services Ltd, in its initiating coverage report on Raymond Lifestyle, recommended a “buy” on the company’s shares, stating that it expected the company to deliver an 11% compound annual growth rate in revenue and 15% CAGR in profit after tax over FY24-27. It set a target share price of ₹3,200 based on 30x the company’s September 2026 P/E ratio. This implies a return of 37% from current levels.

Note: We have relied on data from www.Screener.in as well as company’s presentation throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Mohit Bhambhani is a seasoned financial professional with over 13 years of experience in the field of financial research and corporate advisory. He also has substantial experience in Indian stock markets. With an analytical approach, he studies the performance of companies deeply, bringing value to the readers.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

But let’s begin by understanding Raymond Lifestyle’s various business segments and its competitors in each of those.

Branded textiles

Raymond is well-known for its worsted suiting fabrics, including poly-wool, all-wool, silk, and other blended fabrics used in making garments such as suits and its shirting fabrics, such as cotton and linen. The company has about a 65% market share in the worsted suiting segment. Competitors in this consumer-facing space include Arvind Ltd and Vardhman Ltd.

Branded textiles are Raymond’s highest revenue contributor, accounting for about 50% of its topline in 2023-24. The company’s branded textile unit reported revenue of ₹3,449 crore for FY24, with an Ebitda margin of 20.5%. The segment is clearly a cash cow for the company.

Branded apparel

Raymond sells apparel under four brands to consumers. Its Raymond Ready to Wear and Park Avenue brands offer formal apparel. ColorPlus offers trendy casual and formal apparel, and Parx sells casual clothing for young people.

The Raymond Shop, which was started in 1958, has more than 1,100 stores across 380 towns and cities in India, selling these four brands.

The company’s Ethnix by Raymond brand includes ethnic wear such as sherwanis, kurtas, and jackets, which are sold in 114 stores. According to chairman Gautam Singhania, Raymond plans to add at least 100 Ethnix by Raymond stores in FY25.

The company also sells customized suits, jackets, and shirts to customers through its Raymond Made-to-Measure business.

Raymond’s branded apparel business is its second-largest segment. In FY24, it contributed about 23% of the company’s total revenue, with an Ebitda margin of about 11.5%.

Its main competitors in this segment are Arvind, Aditya Birla Fashions and Retail Ltd, Tata Group’s Trent Ltd, and Shoppers Stop Ltd for ready-made apparel; and Vedant Fashions for ethnic wear. However, these competitors also offer women’s wear.

Garmenting

Raymond’s garmenting business supplies ready-made clothes to multinational brands through its subsidiaries—Silver Spark Apparel Ltd for suits, EverBlue Apparel Ltd for jeanswear, and Celebrations Apparel Ltd for shirts. Competitors in this segment include Arvind Ltd, Gokaldas Exports Ltd, and KPR Mill Ltd.

The garmenting business contributed nearly 15% of Raymond’s total revenue in FY24, with an Ebitda margin of 10.3%.

High-value cotton shirting

Raymond Group sells high-quality cotton and linen fabrics to both domestic and international brands. This segment contributed about 12% of its total revenue in FY24, at an Ebitda margin of 11.4%.

Raymond Home

The group launched Raymond Home in 2013 to sell home textile products such as aprons, bedsheets, blankets, bathrobes, comforters, and table linen. Competitors in this space include Welspun Living Ltd and Trident Ltd.

Projections

Raymond Group’s decision to demerge into three listed entities—Raymond Ltd, Raymond Lifestyle Ltd, and Raymond Realty Ltd—and its growth projections reflect its desire to increase market share.

From about a 65% share in worsted suiting fabrics and a 5% share in ethnic men’s wear, the company is committed to increasing its reach by adding more than 650 retail stores over the next 3 years, with over 100 stores specifically for Ethnix by Raymond in FY25. The expansion will be mainly in Tier 1 and 2 cities and selectively in Tier 3 and 4 markets.

The company expects steady revenue growth of 12-15% over the next few years. This, in turn, is expected to double its Ebitda by 2028, per its growth guidance provided at its investor conference on 17 September. The company expects to lower its net working capital days to 60 from the current 76 and generate annual free cash of ₹600-700 crore.

Key financials

Raymond Lifestyle reported net revenue of ₹6,691 crore for the year ended March, adjusted for intersegment elimination and other income of ₹210 crore. With a gross margin of 46%, an Ebitda margin of 16.3%, and a profit-after-tax margin of 7.0%, it reported 97 inventory days and a net cash surplus of ₹227 crore as of 31 March.

The company’s operational return on capital employed was 31.7%, and operational return on equity was 10.4%.

As of September, promoters held about 54.7% of the company’s shares. Foreign institutional investors held about 12.6% of the shares, domestic institutional investors about 7.9%, and the public about 24.8%.

Comparison with peers

Multiple business segments, specifically those focused on men’s wear, make Raymond Lifestyle a unique company. Let’s now consider its key competitors across segments.

View Full Image

.

Raymond Lifestyle has the lowest price-to-earnings (P/E) ratio among its peers, and a better return on capital employed ratio, which shows the company’s profitability and capital efficiency.

Now getting to the question of whether Raymond Lifestyle can trigger a 37% rally. For this, the company is expanding its network of stores and counters as well as its product range, and expects to double its Ebitda by 2028. This is a positive sign for the company at large.

Also, adding ethnic wear, sleepwear and innerwear to its portfolio will increase its revenue and margin in the coming years.

In October, Motilal Oswal Financial Services Ltd, in its initiating coverage report on Raymond Lifestyle, recommended a “buy” on the company’s shares, stating that it expected the company to deliver an 11% compound annual growth rate in revenue and 15% CAGR in profit after tax over FY24-27. It set a target share price of ₹3,200 based on 30x the company’s September 2026 P/E ratio. This implies a return of 37% from current levels.

Note: We have relied on data from www.Screener.in as well as company’s presentation throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Mohit Bhambhani is a seasoned financial professional with over 13 years of experience in the field of financial research and corporate advisory. He also has substantial experience in Indian stock markets. With an analytical approach, he studies the performance of companies deeply, bringing value to the readers.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

But let’s begin by understanding Raymond Lifestyle’s various business segments and its competitors in each of those.

Branded textiles

Raymond is well-known for its worsted suiting fabrics, including poly-wool, all-wool, silk, and other blended fabrics used in making garments such as suits and its shirting fabrics, such as cotton and linen. The company has about a 65% market share in the worsted suiting segment. Competitors in this consumer-facing space include Arvind Ltd and Vardhman Ltd.

Branded textiles are Raymond’s highest revenue contributor, accounting for about 50% of its topline in 2023-24. The company’s branded textile unit reported revenue of ₹3,449 crore for FY24, with an Ebitda margin of 20.5%. The segment is clearly a cash cow for the company.

Branded apparel

Raymond sells apparel under four brands to consumers. Its Raymond Ready to Wear and Park Avenue brands offer formal apparel. ColorPlus offers trendy casual and formal apparel, and Parx sells casual clothing for young people.

The Raymond Shop, which was started in 1958, has more than 1,100 stores across 380 towns and cities in India, selling these four brands.

The company’s Ethnix by Raymond brand includes ethnic wear such as sherwanis, kurtas, and jackets, which are sold in 114 stores. According to chairman Gautam Singhania, Raymond plans to add at least 100 Ethnix by Raymond stores in FY25.

The company also sells customized suits, jackets, and shirts to customers through its Raymond Made-to-Measure business.

Raymond’s branded apparel business is its second-largest segment. In FY24, it contributed about 23% of the company’s total revenue, with an Ebitda margin of about 11.5%.

Its main competitors in this segment are Arvind, Aditya Birla Fashions and Retail Ltd, Tata Group’s Trent Ltd, and Shoppers Stop Ltd for ready-made apparel; and Vedant Fashions for ethnic wear. However, these competitors also offer women’s wear.

Garmenting

Raymond’s garmenting business supplies ready-made clothes to multinational brands through its subsidiaries—Silver Spark Apparel Ltd for suits, EverBlue Apparel Ltd for jeanswear, and Celebrations Apparel Ltd for shirts. Competitors in this segment include Arvind Ltd, Gokaldas Exports Ltd, and KPR Mill Ltd.

The garmenting business contributed nearly 15% of Raymond’s total revenue in FY24, with an Ebitda margin of 10.3%.

High-value cotton shirting

Raymond Group sells high-quality cotton and linen fabrics to both domestic and international brands. This segment contributed about 12% of its total revenue in FY24, at an Ebitda margin of 11.4%.

Raymond Home

The group launched Raymond Home in 2013 to sell home textile products such as aprons, bedsheets, blankets, bathrobes, comforters, and table linen. Competitors in this space include Welspun Living Ltd and Trident Ltd.

Projections

Raymond Group’s decision to demerge into three listed entities—Raymond Ltd, Raymond Lifestyle Ltd, and Raymond Realty Ltd—and its growth projections reflect its desire to increase market share.

From about a 65% share in worsted suiting fabrics and a 5% share in ethnic men’s wear, the company is committed to increasing its reach by adding more than 650 retail stores over the next 3 years, with over 100 stores specifically for Ethnix by Raymond in FY25. The expansion will be mainly in Tier 1 and 2 cities and selectively in Tier 3 and 4 markets.

The company expects steady revenue growth of 12-15% over the next few years. This, in turn, is expected to double its Ebitda by 2028, per its growth guidance provided at its investor conference on 17 September. The company expects to lower its net working capital days to 60 from the current 76 and generate annual free cash of ₹600-700 crore.

Key financials

Raymond Lifestyle reported net revenue of ₹6,691 crore for the year ended March, adjusted for intersegment elimination and other income of ₹210 crore. With a gross margin of 46%, an Ebitda margin of 16.3%, and a profit-after-tax margin of 7.0%, it reported 97 inventory days and a net cash surplus of ₹227 crore as of 31 March.

The company’s operational return on capital employed was 31.7%, and operational return on equity was 10.4%.

As of September, promoters held about 54.7% of the company’s shares. Foreign institutional investors held about 12.6% of the shares, domestic institutional investors about 7.9%, and the public about 24.8%.

Comparison with peers

Multiple business segments, specifically those focused on men’s wear, make Raymond Lifestyle a unique company. Let’s now consider its key competitors across segments.

View Full Image

.

Raymond Lifestyle has the lowest price-to-earnings (P/E) ratio among its peers, and a better return on capital employed ratio, which shows the company’s profitability and capital efficiency.

Now getting to the question of whether Raymond Lifestyle can trigger a 37% rally. For this, the company is expanding its network of stores and counters as well as its product range, and expects to double its Ebitda by 2028. This is a positive sign for the company at large.

Also, adding ethnic wear, sleepwear and innerwear to its portfolio will increase its revenue and margin in the coming years.

In October, Motilal Oswal Financial Services Ltd, in its initiating coverage report on Raymond Lifestyle, recommended a “buy” on the company’s shares, stating that it expected the company to deliver an 11% compound annual growth rate in revenue and 15% CAGR in profit after tax over FY24-27. It set a target share price of ₹3,200 based on 30x the company’s September 2026 P/E ratio. This implies a return of 37% from current levels.

Note: We have relied on data from www.Screener.in as well as company’s presentation throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Mohit Bhambhani is a seasoned financial professional with over 13 years of experience in the field of financial research and corporate advisory. He also has substantial experience in Indian stock markets. With an analytical approach, he studies the performance of companies deeply, bringing value to the readers.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

Domestic brokerage house Motilal Oswal Financial Services (MOSL) initiated coverage on Raymond Lifestyle, a recent spin-off from Raymond Ltd, with a ‘buy’ rating and a target price of ₹3,200, suggesting an upside potential of over 35 per cent for the stock.

Following the announcement, shares of Raymond Lifestyle surged more than 5.5 per cent in Monday’s trading session. MOSL projects that the company’s revenue and net profit will grow at a compounded annual growth rate (CAGR) of 11 per cent and 15 per cent, respectively from FY24 to FY27.

Also Read | Top 5 stocks in the plastic and tyre recycling ecosystem

“Although the valuation of Raymond’s Lifestyle (RLL) business has almost doubled since the demerger, the stock is currently trading at a relatively lower P/E and an EV/EBITDA (pre-Ind-AS-116) of 25x and 16x on FY26E, respectively. The valuation is significantly lower than that of our Coverage Universe and other retail and discretionary companies, which are valued at an EV/EBITDA of ~35-40x on FY26E. While RLL benefits from strong brand affinity, its valuation has been impeded by sluggish execution in the past (volatility in PAT growth over FY10-20). However, as RLL continues to exhibit a positive growth trajectory, characterised by revenue/PAT CAGR of 11%/15% over FY24-26E, we believe valuations could re-rate,” said the brokerage.

“Additionally, we anticipate a return on invested capital (ROIC) of 24%, 26%, and 30% in FY25, FY26, and FY27, respectively. With improved FCF generation, RLL could look to increase shareholder returns through dividends,” it added.

Raymond Lifestyle emerged as a standalone entity after the demerger from Raymond Ltd, positioning itself as a pure-play lifestyle company. With a strong presence in the men’s wear segment, RLL commands a significant market share of around 65 per cent in worsted suiting. Its portfolio includes a wide range of branded textiles, operating in both B2B and B2C segments. The company also boasts several popular apparel brands, such as Park Avenue, ColorPlus, and Ethnix by Raymond, catering to formal, casual, and ethnic wear categories. Notably, RLL holds about 5 per cent of the men’s wedding wear market, showcasing its prominence in the sector.

Also Read | Dolly Khanna pares stake in THIS multibagger stock. Shares hit 5% lower circuit

In terms of stock performance, Raymond Lifestyle was listed on the NSE on September 5 at ₹3,020. The stock has gained over 17 per cent from its post-listing low of ₹2,081. However, it still trades below its listing day close of ₹2,869. Despite this, analysts remain optimistic about the stock’s future, supported by the company’s solid brand presence, wide distribution network, and ambitious growth plans.

Investment Rationale

MOSL highlighted several growth drivers for RLL, including its fast-paced expansion in branded apparel, targeting a doubling of its exclusive brand outlets (EBOs). The company is also positioned to benefit from Bangladesh+1 and China+1 trends in B2B garmenting, it said. Additionally, the launch of new categories like innerwear and sleepwear as well as a shift towards casualisation and premiumisation of its product portfolio are expected to contribute to its growth, said MOSL. Enhanced sourcing efficiencies due to scale could further improve its operating leverage.

In recent years, Raymond Group has undertaken strategic initiatives such as demerger of its lifestyle and real estate businesses, restructuring of its engineering division, and sale of its FMCG business. These moves have streamlined the group into distinct listed entities focused on lifestyle, real estate, and engineering, aimed at enhancing shareholder value. Each business is professionally managed with a focus on maintaining a net cash balance sheet, optimising costs, and effectively managing working capital.

Also Read | Dharmesh Shah recommends these two stocks to buy today – October 21

Despite historically facing challenges related to growth, profitability, and a high working capital cycle, RLL has made significant progress, the brokerage said, adding that it has improved its working capital management, achieved a net cash position ahead of schedule, and enhanced its pre-IFRS EBITDA margins through store rationalisation and cost control measures.

Under the leadership of Sunil Kataria, former GCPL executive, RLL’s margins have improved to approximately 12 per cent in FY24, up from single-digit levels between FY17 and FY20. Going forward, RLL is focused on accelerating growth in branded apparel, expanding its network, and introducing new categories such as sleepwear and innerwear, alongside scaling up its Ethnix by Raymond brand.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of Mint. We advise investors to check with certified experts before taking any investment decisions.